Funding Advisory Hub

Our Funding Advisory Hub, curates insights and expertise together in one place, to assist your company in raising finance.

Technology, Media and Telecommunications

Our dedicated Technology team can support your business locally, nationally, and internationally.

Coronavirus Business Interruption Loan Scheme

4th April 2020

UPDATED FOR BOUNCE BACK LOANS INTRODUCED ON 4 MAY 2020.

NOTE: CBILS closes for new applicants from 30 September 2020 and Bounce Back loans close on 4 November 2020.

The Coronavirus Business Interruption Loan Scheme (CBILS) provides financial support to smaller businesses (SMEs) across the UK that are losing revenue, and seeing their cashflow disrupted, as a result of the COVID-19 outbreak. The scheme is a part of a wider package of government support for UK businesses and employees and is provided by the British Business Bank.

The British Business Bank’s CBILS facilitates business finance to smaller businesses that are viable but unable to obtain finance due to having insufficient security to meet the lender’s normal requirements. In this situation, CBILS provides the lender with a government-backed 80% guarantee against the outstanding facility balance.

CBILS supports a wide range of business finance products, including term loans, overdrafts, invoice finance and asset finance. To be eligible for support via CBILS, the small business must satisfy the following criteria:

- Be UK based, with turnover of no more than £45 million per annum.

- Operate within an eligible industrial sector (a small number of industrial sectors are not eligible for support).

- Have a sound borrowing proposal which, were it not for the current pandemic, would be considered viable by the lender, and for which the lender believes the provision of finance will enable the business to trade out of any short to medium term difficulty.

An accredited lender can use CBILS to help a borrower access from £50,001 (was £25,000) to £5.0 million with an interest free repayment period of 12 months. In addition, the government will cover any lender-levied set up fees. Finance terms are from three months up to six years for term loans and asset finance facilities, and up to three years for overdraft and invoice finance. It is important to note that the borrower always remains 100% liable for the debt.

Personal guarantees will not be required for loans of up to £250,000. For loans over this amount, personal guarantees may still be required at the lender’s discretion, but they will exclude the borrower’s Principal Private Residence and will be limited to 20% of any amount outstanding on the CBILS lending after any other recoveries from business assets.

The scheme was further enhanced on 4 April 2020 (details here) to provide a government guarantee of 80% to banks making loans of up to £25m to businesses with an annual turnover of between £45m and £500m. Further details are available are available in our article on the Coronavirus Large Business Interruption Loan Scheme

Interaction with Bounce Back loans

As a result of the new Bounce Back loans launched on 4 May 2020, which allow up to £50,000 to be borrowed, the minimum facility for overdrafts and loans under CBILS increased to £50,001 to avoid overlap.

Any customer with a CBILS loan or overdraft of £50,000 or less will be able to switch that facility to a Bounce Back loan should they choose to do so over the next few months. This change to the minimum facility size will not apply to asset finance and invoice finance CBILS facilities.

Applying for CBILS

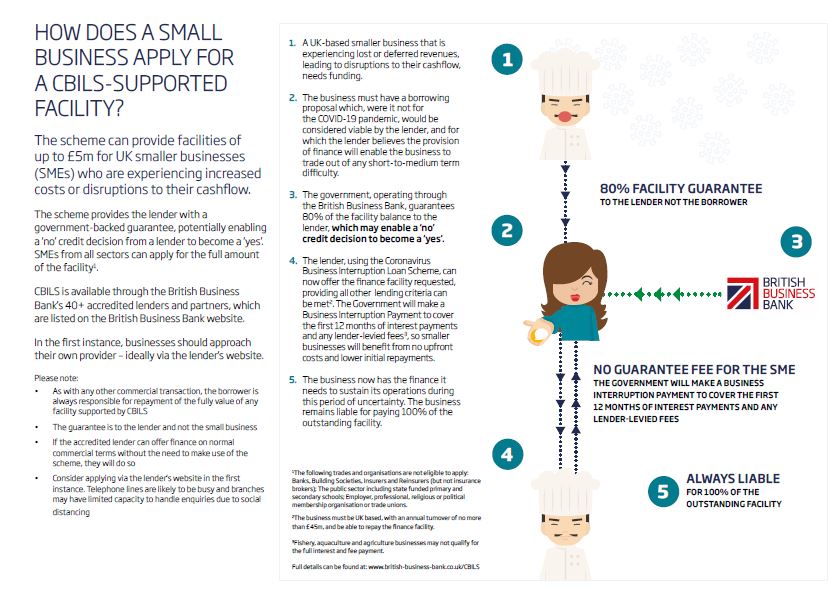

To apply for a CBILS-backed facility, businesses should, in the first instance, approach one of the 40+ accredited lenders with their borrowing proposal. If the accredited lender can offer finance on normal commercial terms without the need to make use of the scheme, they will do so. Where the small business has a sound borrowing proposal but insufficient security, the lender will consider the business for support via the scheme. The following infographic highlights how the scheme will work (infographic courtesy of the British Business Bank):

The British Business Bank has now announced details of the scheme which can be found here.

Whilst this is a crucial source of funding, businesses will still need to prepare a considered funding application. Having an up to date business plan, management accounts and cash flow forecasts available will all be critical to securing appropriate funding for your business during the pandemic.

Capitalise

Bishop Fleming has a team of fundraising specialists ready to advise clients through Coronavirus. As a partner of Capitalise, we have access to 100+ lenders to provide businesses with the opportunity to secure the right kind of funding. Our Capitalise team will support you through all stages of the funding process.

Find out more about raising finance through Capitalise here.

Key contacts